- Hits: 2110

How to select the right Mutual Fund?

I had a question from one of my client regarding housing loan. He wanted to opt for a housing loan without making any changes in his existing investments and his insurance. After almost an hour of discussion he requested me to write an article for others to understand the relationship between Loan and Insurance.

Dear friends, loan is a liability while insurance is an asset. One may even call it a contingent asset. When we take a loan we create a liability and an asset (That is what we think). If we take loan for a vehicle it can be called an asset but asset depreciates fast and involves running cost. When we talk about property it again has high maintenance cost plus it will transfer in your name once the entire loan is repaid. So when we take a loan, we are creating a liability. To balance this liability we must create an asset. That asset is insurance.

Think of a housing loan whose installments are due and consequences that the family will have to face in your absence. Will your family recover from mental trauma, financial loss in the form of lost income, and loss of house due to inability to pay installments? For all those who have outstanding housing loan please upgrade your insurance. The amount must be such that its interest can cover the installment amount. This insurance must be over and above an insurance 3 times your yearly income.

Dear friends change your perception towards genuine insurance planners and agents. They are not to just sell insurance but they are there to provide you right advice so that you and your family live a constant standard of living under whatsoever conditions.

If you are paying a loan or planning to take a loan; and are not insured, contact us today. Special plans are available for such individuals.

Hardik Baxi,

Baxi Investment

Yes, you heard it right. We all save and that is where we usually stop. The problem is we have lot much biasness in our minds. The first being,

1. Knowledge biasness, we have lack of knowledge of what to do with savings. So we either don’t save or we just save and don’t invest or invest in FD as it is the only instrument we understand.

2. Information biasness, we believe when certain people say something. It begins from our family members who always look at banks as ultimate savings & investment option.

3. Incentive biasness, I have heard many savings channelized into non-productive areas just for getting one time share of income from agents. Remember, the agent who has to share commission is like getting a Parle-G at discount. It’s just not possible as already there are very low margins. So if you get an incentive just BEWARE of such investment option.

4. Simplification biasness, we save because it’s simple, we don’t invest because its complex.

5. Bandwagon biasness, we save or not save just because others are saving or not saving.

Still there is much biasness which we can talk about. Todays’ article is to make everyone understand that real wealth is created in investing and not just saving. Savings have to be invested which create an asset. That asset may be financial or physical which earns money in form of interest or capital appreciation. If we just save and not invest, money does not earn anything and we lose purchasing power of our hard earned money.

So stop just saving and start investing. If you have any biasness you can call on +91-7990290560. I will help you overcome your biasness and clear all of your confusions about investment. Start with SIP of Rs. 500/month and you will not feel any difference in your budget. If we lose a Rs. 500 note do we moan? Do we think all the time about it? Than why can’t we start SIP of Rs. 500 and forget about it? I am sure you will regret after some time why did I just forget Rs. 500 and not Rs. 5000.

Indians have always been crazy about the things happening in western world. We blindly follow them without using our brains. We follow what we see and what we see may not be what it actually is.

One such trend which is visible now is making children independent to live their lives the way they want. It is not a bad idea. But have we realised that the western parents plan for their retirement first and then make children independent? We live with mixed mind-set of making children free according to western culture and then not planning our retirement and expecting that the children will support us. These are two contradictory thoughts we live with.

So now whether we want to separate the children or not it’s high time we have another child who will take care of us when we grow old and support us in times of need. This child will remain loyal and be present in times of need. He will not leave us for his better life. The benefit of this another child is one does not even need to marry for having it.

Let us meet this child.

This child is LIC. By investing Rs. 500000 today you can get secure income of Rs. 1,69,000 a year and a risk cover of almost Rs. 80 lakhs to Rs. 2.77 crs. This is available till 100 years of age.

If you are interested to understand the plan or plan your retirement with assured returns call Baxi Investment today on +91-7990290560. Remember 5,00,000 today can fetch you Rs. 1,69,000 from 61 to 100 years of age and guaranteed death benefit of up to 2.77 crs depending on age.

Hardik Baxi

Baxi Investment

Most of us visit our family doctors as we trust them the most. But what happens when the doctor prescribes us a wrong medicine? It gives us unwanted outcome in the form of side effects and uncured ailment. What do we do next? We again talk to him about new problems and he changes the medicine. But what if your doctor insisted that he is correct and he knows what you need?

Same thing happens with our investment advisers. They have knowledge of few investment options and a few mutual funds, they will prescribe you with some instrument based on their limited knowledge which will not suit you. On complaining about side effects they make you understand something or the other. Do you feel same thing has happened to you or is happening with you?

If your adviser does not know you he must ask details about your education, current sources of income, family background, assets owned, investments made, family members, dependants, and much more. Your investment objectives and constraints will serve as major guidelines to select the investment option.

Has your adviser ever asked these things to you if he does not know your background? If the answer is no, it means you will always get a wrong medicine and you will always suffer from some or the other side effects of wrong investment.

If you have experienced the above or want to get a health check of your investments feel free to call and fix a meeting.

Feel free to call on +91-7990290560

Mr. Hardik Baxi,

Baxi Investment

Yes, you heard it right. We all save and that is where we usually stop. The problem is we have lot much biasness in our minds. The first being,

1. Knowledge biasness, we have lack of knowledge of what to do with savings. So we either don’t save or we just save and don’t invest or invest in FD as it is the only instrument we understand.

2. Information biasness, we believe when certain people say something. It begins from our family members who always look at banks as ultimate savings & investment option.

3. Incentive biasness, I have heard many savings channelized into non-productive areas just for getting one time share of income from agents. Remember, the agent who has to share commission is like getting a Parle-G at discount. It’s just not possible as already there are very low margins. So if you get an incentive just BEWARE of such investment option.

4. Simplification biasness, we save because it’s simple, we don’t invest because its complex.

5. Bandwagon biasness, we save or not save just because others are saving or not saving.

Still there is much biasness which we can talk about. Todays’ article is to make everyone understand that real wealth is created in investing and not just saving. Savings have to be invested which create an asset. That asset may be financial or physical which earns money in form of interest or capital appreciation. If we just save and not invest, money does not earn anything and we lose purchasing power of our hard earned money.

So stop just saving and start investing. If you have any biasness you can call on +91-7990290560. I will help you overcome your biasness and clear all of your confusions about investment. Start with SIP of Rs. 500/month and you will not feel any difference in your budget. If we lose a Rs. 500 note do we moan? Do we think all the time about it? Than why can’t we start SIP of Rs. 500 and forget about it? I am sure you will regret after some time why did I just forget Rs. 500 and not Rs. 5000.

With March ending around the corner most of the individuals are busy evaluating investment options for their tax planning. Different advisors giving different advice depending on commission they get from your investment. So the question is which investment option to choose?

BEST OPTIONS U/S 80C

– Investment in PPF – Has 15 year lock in

– Employee’s share of PF contribution – Not all private employers provide it

– Life Insurance Premium payment – Long lock in depending on term chosen

– Principal Repayment of home loan – One has to buy property for this benefit

– Investment in Sukanya Samridhi Account – A daughter is must

– ULIPS – Bad History of returns

– ELSS – Shortest lock in of 3 years and average of 12%+ returns over long term

– Five year deposit scheme – Lock in of 5 years

The dilemma is which option to choose?

No doubt about ELSS as it is the best performing investment option for tax planning with least lock in. However, the question is should you invest in ELSS? All financial advisors will suggest ELSS all insurance agents will suggest insurance, those not involved in financial service business will advise PPF and Sukanya Samriddhi and you will get a new advice and experience from each one of your friends and relatives whom you talk with.

Buy sorry to tell you all are right in their opinions but wrong for you. Why? Because the tool you select depends on your spending habits. I have seen people investing in ELSS just because they can use the money in 3 years, for such people ELSS is worst option. There are people who invest for 35 years with LIC with risk-free moderate returns, for such people ELSS is the best option. Select your investment option based on your spending habit.

If you are thoughtless and extravagant in spending, go for long term options like LIC policies. If you are a thoughtful spender go for ELSS option.

Remember LIC offers plans with 19%-21% annual returns too. It is just that we are not aware about them. For knowing such plan read more.

Disability Insurance in India: How to get it!

Let’s learn what disability insurance is and how to be insured for disability.

Insuring one’s ability to keep earning livelihood is of paramount importance. Accidental disability can render anyone temporarily or permanently disabled for life. This is why we all look for an insurance policy for disability. However, getting disability insurance in India is not a straightforward task. In fact there are no separate insurance policies available especially to cater for the events of disability. So, many people wonder how to get such an insurance policy. Today I am going to write a few facts on this subject.

What is Disability Insurance?

Disability insurance is also known as disability income insurance. It is an insurance policy that covers a person for disability conditions in future. Disability due to accidents and diseases can strike anyone at any time. Such an event may adversely impact one’s ability to earn. A disability insurance policy ensures that if such an event happens, the insured person would get financial assistance. The money got from disability insurance can come handy for treatment and to provide for the dependent family members.

A lot of people do not understand the importance of getting a good disability insurance. People make all sorts of investments but they hardly invest a portion of their income in securing their future against permanent or temporary disabilities.

Depending on the nature of disability, the insurance can provide short-term disability benefits or long-term disability benefits.

How to Get Disability Insurance in India?

As I said earlier, there are no separate insurance policies available for protection against disability. But various Life Insurance and Term Insurance plans come with disability and accident riders. A rider is an add-on for which you will have to pay extra premium. If you opt for disability rider in your insurance plan — then you will receive benefits in case of a disability. Some plans offer benefits only in case of permanent disability whereas some other offer benefits for temporary disability as well.

Disability Insurance often Corresponds to Monthly Income

Yes, the disability rider corresponds to monthly income. One can get an amount equal to their income for a period of 10 years every month. The main advantage of this rider is that disability arising after 180 days of accident is also covered. So even if you get disability later on, you are covered. However the insurance company must be informed as soon as the disability occurs (Standard time is 90 days).

Premium waiver for life insurance policy

Another advantage of LIC disability rider is that post disability the insured does not have to pay any premium for his life insurance policy. The policy continues with all benefits for free.

How LIC defines benefits under disability rider:

In case of Total and Permanent disability arising due to accident an amount equal to accident benefit sum assured will be payable over a period of 10 years in monthly instalments. However, the payment of accident benefit will be subject to an overall limit of Rs.25 lakh under all policies of the Life Assured with the Corporation taken together.

The disability due to accident should be total and such that the Life Assured is unable to carry out any work to earn a living. Following disabilities due to accident are also covered -

a) irrevocable loss of the entire sight of both eyes or

b) amputation of both hands at or above the wrists or

c) amputation of both feet at or above ankles, or

d) amputation of one hand at or above the wrist and one foot at or above the ankle.

Contact us today for securing your future income @ +91-7990290560

Most of us are very much clear when it comes to buying things for ourselves about the performance of product. If we buy a family car we don’t expect it to do wonders on the road. Likewise if we buy a sports car we don’t expect to fit in the entire family. Post purchase we are satisfied because we have rational expectations of performance considering amount spent. But now consider a case where you buy a family car and enter into a race with it. Can you blame the manufacturer for your defeat? The answer is NO. Likewise while purchasing insurance people talk about returns. Many clients ask that does any policy do more than 4.5%? Dear Sir/Madam you are expecting a family car to do 300km/hr which is not possible and you are surely going to be dissatisfied.

All those reading this article please make sure that while buying a life insurance policy please do not ask about returns, look at options available, cover provided, raiders available as we are buying an insurance for life cover and not returns.

Yes, there are plans available which act like MUV (Multi Utility Vehicles) cars which provide insurance + moderate returns. Do not expect these plans to do wonders for you. To know more about such products call us today on +91-7990290560

In today's article I would like to draw your attention on "Why we don't need an insurance policy?"

Insurance in India is majority times sold and not purchased. In most of the sales calls I have done majority people have insurance policy because some of their relative had taken LIC agency and as a result they sold them a policy which they could not refuse. This is a fact which we have to agree upon.

Think of an example where the bread earner is going out of town for a week leaving family behind. The first thing he will do is give money for more than 7 days to the other members in case he is late in returning. But when it comes to Insurance we do not care. We think of one week absence than why don't we think of sudden permanent absence?

For an unmarried person amount of insurance must be at least 5 times annual income depending on dependents while for a married person it must be at least 10 times of annual income.

So now ask your self, Do we need insurance policy? or Do we need to be insured?

While buying insurance the first question comes to our mind is, which insurer to select? this question comes to our mind because of constant advertisements bombarded by private insurers claiming to be the best. People try to act smart by looking at claim ratios of various companies which is a misleading figure because if you compare LIC which had 30 crore+ policies in force while others have not even 10% in force it is obvious figures can not be compared.

One must stick to the giant whose policy is guaranteed for repayment by the Government of India. There is no question of default or closure of company.

So think over are you Insured??? If you want to get your insurance needs assessed do get in touch with us.

Hardik Baxi,

Baxi Investment

Most of the parents are worried about the future of their children and especially the girl child and her marriage. Looking at current social change I personally believe that worry has become less relevant today. However, if still one wants to save for daughters' education & marriage the majority question everyone has is which instrument to choose?

Today we will try to compare and evaluate 2 well known options 1. Sukanya Samruddhi Yojna & 2. Jeevan Tarun Plan

Both plans are guaranteed by the Government of India so they are risk-free. Let us compare features of both the plans.

|

Type |

Sukanya Samriddhi Yojana |

Jeevan Tarun Plan |

|

Type of Investment |

If you are looking for a small investment scheme that will provide you with a good interest rate then SSY is the best option. |

If you are looking for a life cover that will secure the future and also give benefits in the present then LIC has a number of options. |

|

Tenure of maturity |

The total time that is required for the SS scheme to mature is 21 years. |

The time of maturity, of the LIC scheme will depend on the policy that the customer has selected. |

|

Life coverage |

If the depositor dies, the girl in whose name the account has been opened will not get a life coverage benefits. |

The main reason for purchasing the LIC policy is that after the demise of the depositor, the family will get the life coverage benefits |

|

Account holder |

The SS account can only be opened by the parents of the legal guardian. The account can only be opened for a female child. |

Anyone can opt to purchase a LIC policy. The customer will be able to purchase the policy for both a girl and a boy offspring. |

|

Facility of nominations |

The account holder is the only person for whom the account can be opened. There is no facility of nominating anyone else |

When purchasing a LIC policy, the client will be able to nominate two people who will get the money after the demise of the actual client. |

|

Fixed rate of interest |

The interest rate that the SSY is offering will depend on the economic market. It is not fixed. |

Though the rates will differ according to the policy terms and also the market, once you have taken the policy, the rate will remain the same till the maturity date. |

|

Pre-mature withdrawal facility |

Once the female child has attained the 18 years, she will be able to withdraw only 50% of the total amount that has been accumulated in the account. |

Only after the completion of 3 years will the client be able to surrender the LIC policy. |

|

Tax benefits |

The SSY account will get tax benefits under the Section 80C |

The amount invested in the LIC policy will also get tax benefits as per the rules of Section 80 C |

The Verdict:

Both plans are good in their place but when it comes to pre-mature withdrawals in case of emergency Jeevan Tarun is better. Similarly interest rate in SSY is variable so risk of downward shift is always present. Moreover Jeevan Tarun gives a stream of cash flow from age 20-25 which can be useful for higher education fees payment.

Overall one can say that the Jeevan Tarun plan has an upper edge over SSY looking at its flexible features.

To know more feel free to contact on +91-7990290560

Hardik Baxi,

Baxi Investment

An emergency fund is a pool of liquid money set aside for unforeseen expenses like a medical expense or job loss. Having an emergency fund can be the difference between a small bump in your financial life and complete disaster in your entire life.

Many people fail to prepare for the future. Financial security is important for every person. An emergency savings fund can help individuals look forward to the future without worrying about being unprepared for unexpected expenses.

Having an emergency savings fund is critical to the financial security of your family. Learning more about this type of fund can better prepare people to start saving if they have not already done so.

Everyone has a certain set of fixed expenses each month. These bills have to be paid on time to retain excellent credit. Some of these expenses include a mortgage, health insurance, life insurance, car payments, car insurances, home utility bills, food, and automobile gas. Let’s say that a person is living week to week and has no savings at all or has only a very minimal amount in a bank account. If this person suffers a job loss, this could be catastrophic.

That’s why no matter how hard it is to save; an emergency fund must be saved in order to carry a person or family through those tough economic times when not enough income is coming in to pay all the required expenses. People can lose their homes to foreclosure. Renters can be evicted and have no money to stay at a hotel or to re-rent another home. Shelter is a must, as is food, and paying for prescription drugs, and keeping up all of the insurance policies and car payments, otherwise people can have their cars repossessed if they do not make the payments.

So it’s imperative to save a separate emergency fund. One way to do this is to cut back on nonessential items such as eating out every day or buying fancy clothing that people don’t really need. Keep a journal of the items you cut out, and put that money into a savings account each week. As the account starts to grow, you’ll probably start to feel a real sense of accomplishment, and you probably won’t even notice the things that you cut out of your spending.

Paying down debt is also a great way to help grow your savings. As you pay off your loans and credit cards, the money you used to put toward these bills can be set aside in savings where it will grow for you year after year.

How much money to set aside as emergency fund?

Ideally it must be an amount equal to 6 months income.

How to invest emergency fund money?

Always remember that emergency fund has an intention of being useful at any point of time so liquidity is of prime importance. Second comes safety as we cannot afford to lose anything from this fund. Third is it must provide average returns. Liquid funds are the best option. With NJ E-Wealth account one gets this facility without additional cost. The service is available at just a click of mouse or a tap on your mobile screen. One can get returns on daily basis, so if you have money even for 24 hours, you can invest it. Average returns are 6.5% per annum.

To know more about planning and investing your emergency fund contact us today on +91-7990290560

Hardik Baxi,

Baxi Investment.

Hello readers,

The title of today's article is "Buying potatoes from health insurance companies", yes you heard it right. This is how our Indian mentality works. Recently I had 5 sales calls from them there was a group of 3 elderly gentleman looking for health cover. They inquired me regarding plan details, its advantages and limitations. On completion of my presentation they told your company is charging 33000 Rs. while other is charging 27000 Rs. They concluded we do not wish to buy health insurance from your company. They had gathered so that they can bargain the amount of premium the way we bargain with hawkers that if we buy thrice the quantity what discount will you offer us.

The situation was like Mr. A is selling potatoes for 10 Rs. a Kg while Mr. B is selling it at 11 Rs. a Kg and hence we will purchase from Mr. A. People do not understand that the bargaining and hunting for low price strategy is for commodities where all supplies are same. The same strategy cannot be applied for Insurance.

Comparing premiums for same same insured and selecting one with lowest premium is a type of suicide. The insurance market is highly competitive with companies incurring losses or normal profits. None of them can afford to provide more at less price or provide less at more price. The difference in pricing is due to difference in features.

So please those who are reading the article please understand that you have to purchase insurance and not potatoes. The strategy of bargain and less price for same quantity is not applicable here. Here there is a contract which is full of conditions, medical terms, highlighted advantages, undisclosed limitations and much more.

Compare features and not premium as we are buying a serious product and not potatoes.

Hardik Baxi

Baxi Investment

Most of us buy mutual funds but do not know when to sell them. We also do not know which fund to buy? How many funds to buy? When to buy? How to buy? this when and how creates a confusion and the confusion leads to errors in investing.

Today I will try to explain a product which will eliminate all which and how queries.

MARS = Mutual Fund Automated Re-balancing System

It is first and only of its kind advanced mutual fund management system which has predefined rules which help you to keep your mutual funds balanced. The system adjusts proportion of mutual funds in your portfolio to give you the best outcome. The system automatically reduces equity exposure when markets are high and reduces debt exposures when markets are low. The robust and dynamic model strikes optimum balance between risk & return and delivers best outcome.

Firstly I would like to thank you for clicking on the article and reading it. But you better know the answer to this question than I do. Yes, you know it better than I do.

I get about 5 calls/messages every day saying we have determined this time we will save and invest for our better future but none of them turn out to me.

I have few clients who commit monthly savings but than in few months feel pain of fixed monthly outflow for investment.

I have few clients who are fully determined but suddenly need money for buying gift for spouse or children or want to go on unplanned vacation or replacing mobile or vehicle which is working fine.

Above are few examples of people who form 75-80% of investors. I think they have answer of how to succeed without determination that is why they lack determination. I can not achieve financial well being without determination.

When we take a loan, it creates a liability. We remain loyal in repaying the loan as we fear the company may take away the article or take legal actions against us. Now, when we are committed to some asset why cant we have same determination as our determination towards our liability?

This article may seem a casual one but try to understand the profound message hidden within it.

Hardik Baxi,

Baxi Investment.

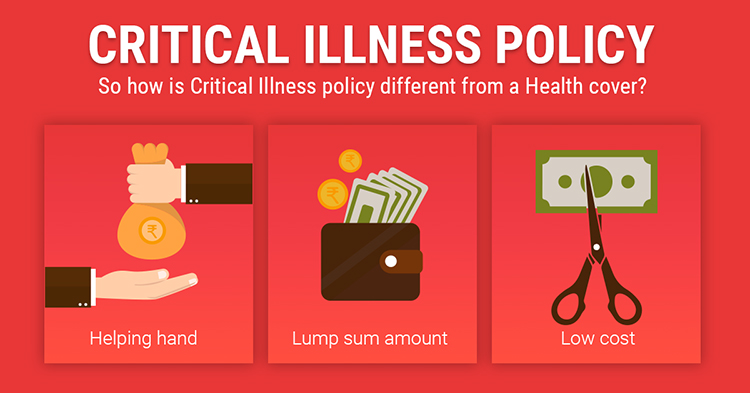

Critical illness is an illness that is a major illness affecting an important organ of the body. Examples of critical illnesses – heart attack, stroke, cancer, kidney, lungs, liver failure etc. The longer that we are living, the more the chances of any of these critical illnesses striking us. 99% of clients that I have met are usually aware of hospitalisation policy, for example, a “Mediclaim” policy.

Critical illness is an illness that is a major illness affecting an important organ of the body. Examples of critical illnesses – heart attack, stroke, cancer, kidney, lungs, liver failure etc. The longer that we are living, the more the chances of any of these critical illnesses striking us. 99% of clients that I have met are usually aware of hospitalisation policy, for example, a “Mediclaim” policy.

They are not aware of the risk of the outgo on account of major illnesses that critically threaten a patient’s life. Critical Illness typically requires ICU, nursing, specialised medicines and tests that are costly. Typical critical illness such as cancer can cost upwards of Rs 20 lakh. Most of the hospitalisation policies for medical treatment do not cover such large amounts. It is therefore important to have a separate insurance policy for the risk of major illness striking us.

The difference between a hospitalisation policy and critical illness policy is this – hospitalisation policy gives you reimbursement of all the hospitalisation costs such as surgery, ICU et cetera. It will not cover many items such as medicines, cost of stay of the relatives, some diagnostic costs, and nursing cost required at home. Sometimes in chronic illness, these other costs are higher than the main surgery or the hospitalisation cost.

Unlike hospitalisation insurance, critical illness policy will pay you a lumpsum upon diagnosis of a critical illness. It is not dependent on submitting hospital bills and is therefore not a reimbursement policy. For example, if one has a critical illness of Rs 30 lakh and one is detected with a major liver disease, he/she will get a lump-sum claim of Rs 30 lakh without requiring any bills or other questions.

Many of the critical illnesses are chronic in nature which means they are present for a long time and require long-term care and treatment. This automatically increases the cost of treatment and burden of this cost falls on the financial savings of the patient.

Today it is a happy development that most health insurance companies offer critical illness plans. There are many life insurance companies who offer critical illness “rider” to be added on to life insurance plans. This money is the cash that will sustain the person for all myriad costs that he/she will have to incur in order to treat herself back to health.

© Copyright 2026 Baxi Investment Website designed by Vanhar Infotech